Credit Score Optimization in 2026: Achieving a 750+ FICO Score with 4 Strategic Moves

Anúncios

The landscape of Credit Score Optimization has shifted significantly in 2026, making the journey to a 750+ FICO score more achievable than ever.

With lenders now prioritizing long-term financial patterns over quick fixes, understanding these new rules is the key to unlocking premium interest rates.

Anúncios

Modern creditworthiness hinges on your ability to navigate updated reporting models that now weigh consistent behaviors more heavily. By fine-tuning your profile against these evolving benchmarks, you can transform your borrowing power and secure a top-tier rating.

Achieving an elite status requires four precise strategic moves tailored to today’s digital-first economy. Stay ahead of the curve by monitoring these critical updates and implementing the proven tactics necessary to dominate the current lending environment.

Understanding the FICO Score Landscape in 2026

The FICO Score remains a cornerstone of financial assessment in the United States, influencing everything from mortgage rates to insurance premiums. As we approach 2026, understanding its nuances becomes even more critical for consumers.

Changes in lending practices and economic indicators continue to subtly shift how credit scores are evaluated and weighted. Staying informed about these evolving dynamics is paramount for effective Credit Score Optimization in 2026.

Anúncios

A 750+ FICO score signifies exceptional creditworthiness, opening doors to the most favorable financial products and terms. This threshold is often seen as the gateway to significant savings over a borrower’s lifetime.

Recent data helps clarify the scope and sequence of events regarding credit health. Analysts highlight short-term signals that deserve attention before broader trends become clear for Credit Score Optimization in 2026.

The Importance of a High FICO Score

A strong FICO score is not merely a number; it is a powerful financial tool that unlocks opportunities. It directly impacts the interest rates offered on loans, potentially saving thousands of dollars over the life of a mortgage or auto loan.

Beyond loans, a high FICO score can influence rental applications, utility deposits, and even employment opportunities in some sectors. It signals financial responsibility and reliability to potential creditors and service providers.

For those aiming for significant financial goals by 2026, such as buying a home or starting a business, a 750+ FICO score is often a prerequisite for the best deals. This makes Credit Score Optimization in 2026 a strategic imperative.

Strategic Move 1: Mastering Payment History

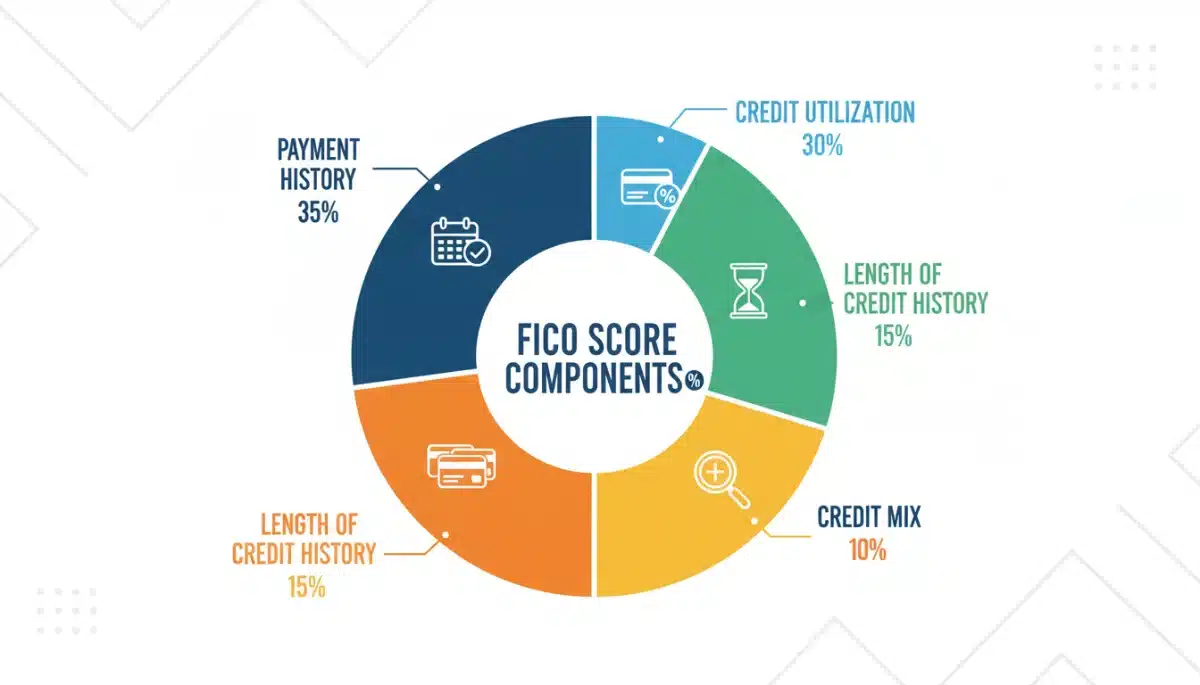

Payment history is the most significant factor in FICO score calculations, accounting for 35% of the total score. Consistently making on-time payments is the bedrock of strong credit health and essential for Credit Score Optimization in 2026.

Even a single late payment can have a disproportionately negative impact, especially on an otherwise stellar credit report. Creditors view late payments as a strong indicator of future risk, which can severely hinder efforts towards a 750+ FICO score.

Establishing automated payments for all credit obligations can be a highly effective strategy to ensure timely payments. This reduces the risk of human error and helps maintain a perfect payment record, crucial for Credit Score Optimization in 2026.

Automating Payments for Consistency

- Set up automatic transfers from your checking account to cover credit card and loan payments.

- Review payment schedules regularly to ensure sufficient funds are available.

- Consider setting payment reminders a few days before the due date as a backup.

Disputes regarding incorrect late payment entries on your credit report must be addressed promptly. Gathering documentation and contacting both the creditor and credit bureaus is vital to rectify errors and protect your payment history.

Strategic Move 2: Optimizing Credit Utilization

Credit utilization, the amount of credit you’re using compared to your total available credit, accounts for 30% of your FICO score. Keeping this ratio low is critical for Credit Score Optimization in 2026, ideally below 30%.

A utilization ratio above 30% can signal to lenders that you might be over-reliant on credit, even if you pay your bills on time. This perception of higher risk can depress your FICO score, making the 750+ goal more challenging.

To effectively manage credit utilization, consider paying down balances aggressively and, if possible, making multiple payments within a billing cycle. This proactive approach can significantly impact your reported utilization for Credit Score Optimization in 2026.

Strategies for Lowering Utilization

- Pay down credit card balances before the statement closing date to ensure a low reported balance.

- Avoid maxing out credit cards, even if you plan to pay them off quickly.

- Consider requesting a credit limit increase if your spending habits necessitate it, but only if you can resist the urge to increase your spending accordingly.

Opening new credit accounts solely for the purpose of increasing available credit should be approached cautiously.

While it can lower utilization, the hard inquiry and new account can temporarily drop your score, necessitating a balanced approach for Credit Score Optimization in 2026.

Strategic Move 3: Cultivating Length of Credit History

The length of your credit history contributes 15% to your FICO score. This factor considers the age of your oldest account, the age of your newest account, and the average age of all your accounts. For Credit Score Optimization in 2026, patience and careful management are key.

Closing old credit accounts, even those you no longer use, can negatively impact the average age of your accounts and shorten your credit history. This can be detrimental to achieving and maintaining a 750+ FICO score.

Maintaining older accounts, even with minimal usage, can be beneficial for your FICO score.

Consider making small, occasional purchases and paying them off immediately to keep these accounts active and contributing positively to your credit history for Credit Score Optimization in 2026.

Preserving and Growing Your Credit Age

Avoid closing your oldest credit accounts, especially if they have a good payment history. These accounts are valuable anchors for your credit age and demonstrate a long history of responsible borrowing.

If you have joint accounts or authorized user accounts, understand how they impact your credit history. While they can boost your score, ensure the primary account holder maintains excellent credit habits.

New credit applications, while sometimes necessary, will lower your average credit age. Strategically space out applications for new credit to minimize their impact on your credit history length, crucial for Credit Score Optimization in 2026.

Strategic Move 4: Diversifying Credit Mix and Limiting New Credit

Your credit mix, which constitutes 10% of your FICO score, refers to the different types of credit accounts you manage, such as revolving credit (credit cards) and installment loans (mortgages, auto loans).

A healthy mix demonstrates your ability to handle various credit types responsibly, aiding Credit Score Optimization in 2026.

While a diverse mix is beneficial, it’s not advisable to open new accounts solely for this purpose. The emphasis should be on responsible management of existing accounts, and allowing a natural diversification as your financial needs evolve.

New credit applications and recently opened accounts also make up 10% of your FICO score. Each hard inquiry can temporarily ding your score, and opening too many new accounts in a short period can be viewed negatively by lenders, impeding your 750+ FICO score goal.

Balancing New Credit with Existing Accounts

- Apply for new credit only when genuinely needed and after careful consideration.

- Consolidate inquiries for similar loans (e.g., mortgage shopping) within a short timeframe, as FICO models often treat them as a single event.

- Focus on managing your current credit effectively before seeking new lines of credit for Credit Score Optimization in 2026.

Monitoring your credit report regularly for unauthorized new accounts is crucial. Identity theft can lead to new accounts being opened in your name, severely damaging your score and requiring immediate action to resolve for Credit Score Optimization in 2026.

Monitoring Your Credit Health Regularly

Regularly checking your credit reports from all three major bureaus (Equifax, Experian, TransUnion) is a non-negotiable aspect of Credit Score Optimization in 2026. This allows you to identify errors, fraudulent activity, and areas for improvement.

Annual free credit reports are available, but many financial institutions and credit card companies now offer free credit score monitoring services. These tools can provide ongoing insights into your credit health and alert you to significant changes.

Disputing inaccuracies on your credit report is a critical step. Even small errors can potentially impact your FICO score, and timely correction ensures your report accurately reflects your financial behavior, aiding your 750+ FICO score objective.

Utilizing Credit Monitoring Services

Many credit card providers offer free access to your FICO score and credit report summaries. Leverage these tools to stay informed about your credit standing without incurring additional costs.

Consider setting up alerts for significant changes to your credit report, such as new accounts being opened or large inquiries. This proactive approach can help you detect and address potential issues quickly.

Understanding the different scoring models, beyond just FICO, can also be beneficial. While FICO is dominant, some lenders use alternative models, and being aware of these can provide a more holistic view of your credit health as you pursue Credit Score Optimization in 2026.

Addressing Derogatory Marks and Collections

Derogatory marks, such as collections, charge-offs, bankruptcies, and foreclosures, can severely impact your FICO score for many years. Addressing these issues proactively is a vital component of Credit Score Optimization in 2026.

For collections, consider negotiating a “pay-for-delete” agreement, where the collection agency agrees to remove the entry from your credit report upon payment. While not always successful, it’s worth exploring this option.

Understanding the statute of limitations for debts in your state is also important. While a debt may be legally uncollectible after a certain period, it can still remain on your credit report for up to seven years, affecting your 750+ FICO score goal.

Strategies for Managing Negative Entries

If you have old debts that are nearing the seven-year mark, avoid making payments on them, as this can restart the clock on their reporting period. Consult with a credit counselor if you are unsure.

For significant derogatory events like bankruptcy, focus on rebuilding your credit through secured credit cards and small installment loans. Demonstrating responsible financial behavior post-event is crucial for Credit Score Optimization in 2026.

Always verify the accuracy of any derogatory mark on your credit report. If you find errors, dispute them immediately with the credit bureaus and provide any supporting documentation you have.

Long-Term Financial Planning and Credit Score Optimization

Achieving a 750+ FICO score by 2026 is not a short-term fix but a result of consistent, disciplined financial planning. Integrating credit health into your overall financial strategy is key for sustained success.

This includes budgeting effectively, building an emergency fund, and making informed decisions about taking on new debt. A holistic approach ensures that your efforts towards Credit Score Optimization in 2026 are sustainable.

Understanding the interplay between your spending habits, savings, and credit behavior is fundamental. Each financial decision has a ripple effect on your credit profile, impacting your journey towards a superior FICO score.

Building a Resilient Financial Foundation

- Create and stick to a realistic budget that prioritizes debt repayment and savings.

- Establish an emergency fund to avoid relying on credit cards for unexpected expenses.

- Educate yourself on personal finance principles to make informed decisions that support your credit goals.

Seeking guidance from a reputable non-profit credit counseling agency can provide personalized strategies and support. They can help you develop a debt management plan and offer advice tailored to your specific financial situation for Credit Score Optimization in 2026.

| Key Strategy | Brief Description |

|---|---|

| Master Payment History | Make all payments on time, every time, to build a strong foundation. |

| Optimize Credit Utilization | Keep credit card balances below 30% of available limits. |

| Cultivate Credit History Length | Maintain older accounts and avoid unnecessary closures. |

| Diversify & Limit New Credit | Manage a mix of credit types and apply for new credit judiciously. |

Frequently Asked Questions About FICO Scores

Payment history is the single most critical factor, accounting for 35% of your FICO score. Consistently making all payments on time is foundational to achieving a 750+ score. Even one late payment can have a significant negative impact on your overall credit health.

Credit utilization, the amount of credit you use versus your total available credit, makes up 30% of your FICO score. Keeping this ratio below 30% is ideal. A lower utilization signals responsible credit management, positively impacting your score for Credit Score Optimization in 2026.

Generally, no. Closing old credit cards can shorten your average credit history length and reduce your total available credit, both of which can negatively impact your FICO score. It’s often better to keep old accounts open, even if you use them infrequently, for Credit Score Optimization in 2026.

It’s advisable to check your credit reports from all three major bureaus at least annually. Many services also offer free credit score monitoring, providing more frequent updates. Regular checks help identify errors or fraudulent activity promptly, crucial for Credit Score Optimization in 2026.

While paying off collections is positive, the impact on your FICO score isn’t always immediate or dramatic. The collection will remain on your report for up to seven years. Negotiating a “pay-for-delete” can be more effective for faster score improvement in Credit Score Optimization in 2026.

What happens now

The journey towards a 750+ FICO score by 2026 demands proactive engagement with your financial health. These four strategic moves for Credit Score Optimization in 2026 are not merely guidelines but actionable steps that, when consistently applied, yield significant results.

As economic conditions and lending standards continue to evolve, staying informed and adaptable will be key to managing and improving your credit standing.

Focus on disciplined payment habits, strategic credit utilization, maintaining a long credit history, and judiciously managing new credit to secure your financial future.